The pace of exits has been glacial. When it comes to your private equity and venture capital investments, you’re writing checks, but you’re not cashing them. So you’re interested in getting liquidity. But how?

You could wait for the IPO market to open up.

You could wait for the M&A market to open up.

Everyone knows that will happen momentarily. Right?

Everyone also knew in 2023 that we were definitely going into recession. So much for that. Everyone also knew there would be three or four rate cuts in 2024. So much for that.

Our view is that nobody knows anything when it comes to macroeconomic forecasting.

So, what if the surge in exits everyone thinks is inevitable is actually you know, evitable? Okay fine, evitable is not a word, but it should be. (It’s a “lost positive.”)

As we noted in our article in Global Corporate Venturing, to know what you want, you have to know what you want. In other words, you have to know what your strategic objectives are in generating liquidity.

If you’re a corporate venture arm, your key objectives may be to preserve your investee relationships, and to avoid a writedown. That would lead you toward one transaction structure.

If you’re an LP grappling with the denominator effect or getting impatient waiting for DPI and your objectives are exclusively financial rather than strategic, that would lead you to a different structure – and a different set of counterparties.

Here’s the (highly simplified) TLDR on three liquidity options:

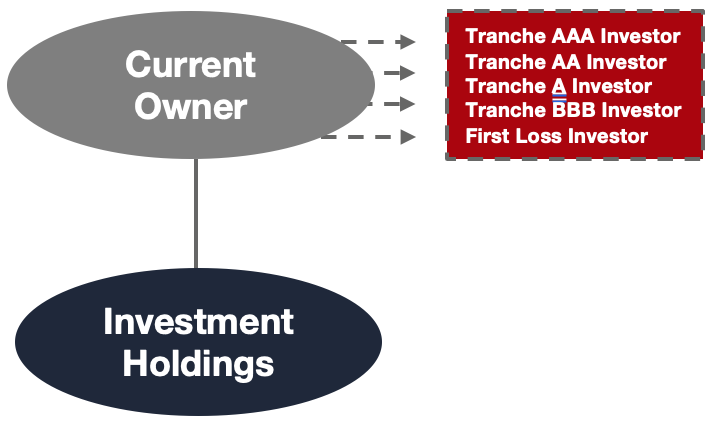

1. Collateralized Fund Obligation.

This is a type of collateralized debt obligation. It’s a loan secured by your private investment holdings, with some upside participation as well. This structure requires ratings agencies like Moody’s to rate the creditworthiness of different tranches of debt participation.

Proceeds above the required debt payouts go to an equity investor who is junior to the debtholders. It requires compliance with over-collateralization and other covenants. While it’s an increasingly popular structure, because of the high degree of complexity it’s better suited to financial institutions rather than say, the corporate venture arm of a CPG firm.

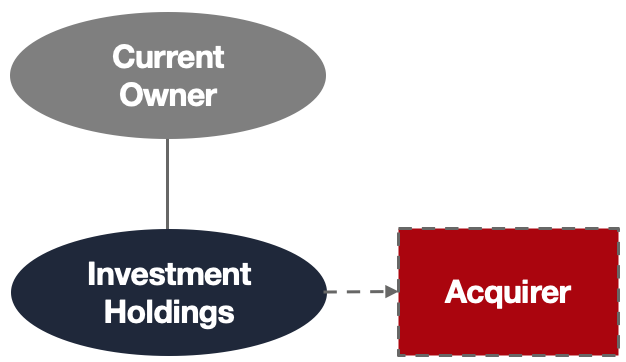

2. Secondary Sale.

This is the most widely understood of the three options. The current owner sells its investments to an acquirer. The acquirer inevitably pays a discount. (In this case it really isn’t evitable).

Prevailing discounts across venture capital are 32% of NAV, and because it’s a sale, there’s a “pricing event.” It therefore requires the current owner to take a writedown for the difference between the NAV on the balance sheet, and the sale price. The exiting owner loses their portfolio company relationships, but they also get a larger total payment relative to the strip sale described below because they’re exiting entirely and giving up all their upside.

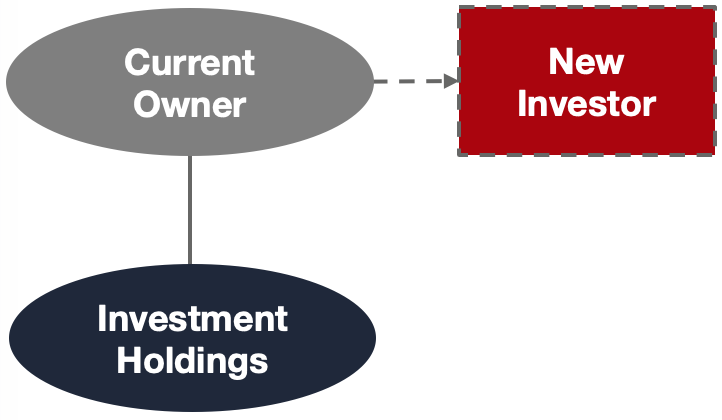

3. Strip Sale.

A strip sale is a profit participation where a new investor pays up front for a share of future proceeds generated by the portfolio. Unlike a secondary sale, the current owner keeps their portfolio company relationships.

The main change from the status quo is that the current owner now has a new financial partner who will receive some of the upside. The current owner keeps its portfolio company ownership and governance, and keeps some upside. Because the current owner keeps some of the upside, it results in a smaller total payment than in a secondary sale where all upside is surrendered. But critically, it’s not a pricing event, so there is usually no writedown for the current owner. For corporate venture arms this is often the most attractive option.

So – know what you want, so you know what you want – and keep your key stakeholders gruntled.

PS if London is calling, please say hello at the Global Corporate Venturing Symposium in London beginning June 24th.

Helping you understand your best options and generating liquidity for your holdings is what we do. If you’d like to learn more, don’t hesitate to schedule an introductory conversation or reach out via email.