Why would an investor want to buy into a corporate venture portfolio?

Aren’t corporate venture arms (“CVCs”) a rounding error on VC investing?

Don’t they care only about “strategic returns” and ignore actual, you know, financial returns?

Aren’t they um, bad at investing?

Actually, no, no and no.

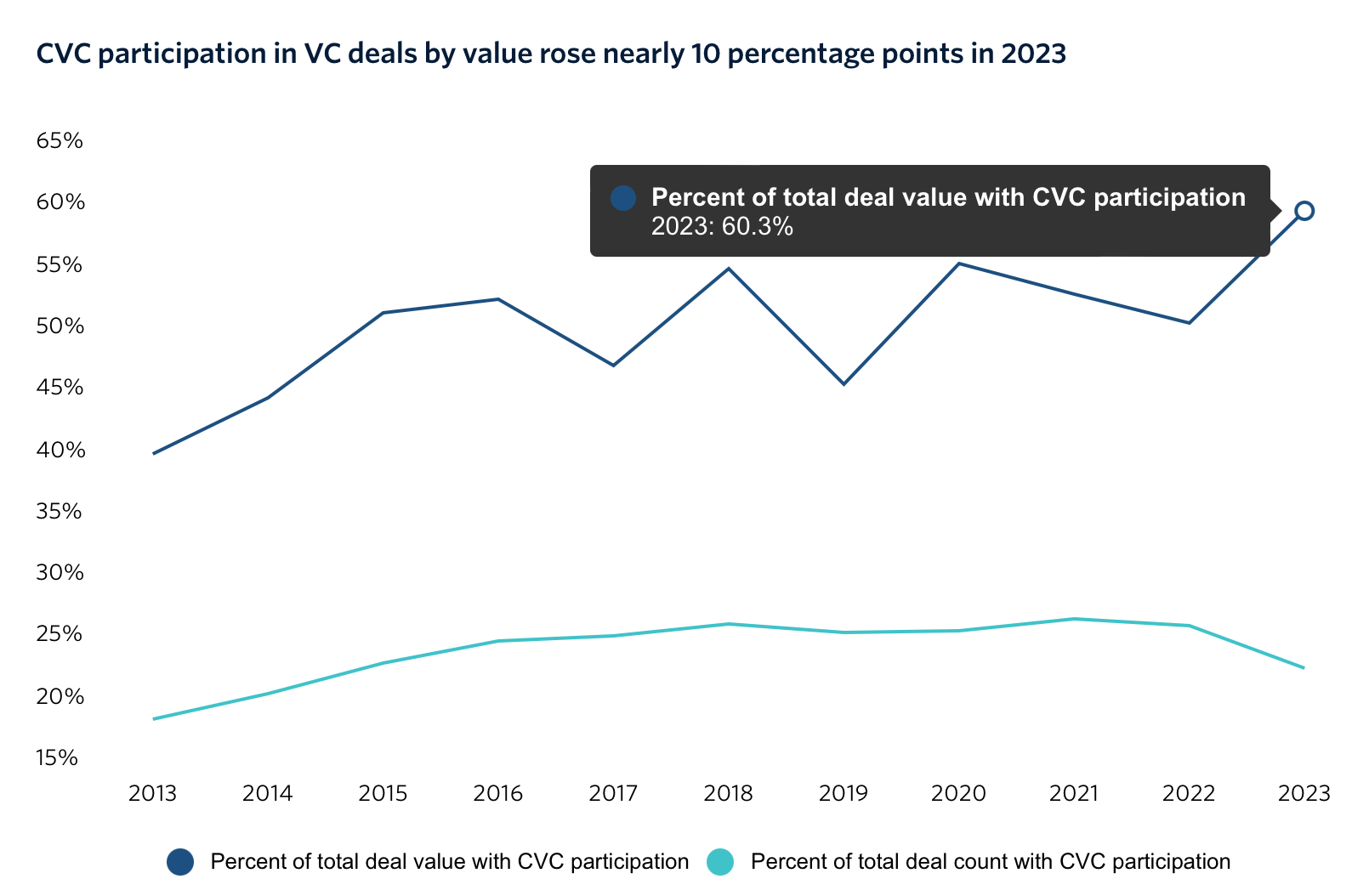

Aren’t CVCs a rounding error in the overall venture ecosystem?

Actually, CVC participation in venture deals is at a ten year high. In 2023, they were involved in more than 60% of all VC deals, measured by deal value.

And they’re not a rounding error on exits, either. In the champagne years of 2021 when VC exits were at their peak, CVCs were investors in 43% of exit transactions – and those exits represented 84% of the total exit value generated.

Don’t they ignore financial returns?

No again. Yes, part of their reason for being is to deliver strategic returns to the corporate parent. But CVCs tend not to survive for very long if they deliver only squishy, hard-to-measure strategic benefits. That’s why over 55% of CVCs are evaluated exclusively on financial metrics. (33% report a mix of financial and non-financial metrics; only 13% report exclusively non-financial metrics.)

But aren’t CVCs bad at investing? Or at least, worse than conventional VCs?

Actually by some measures, they’re better than conventional VCs.

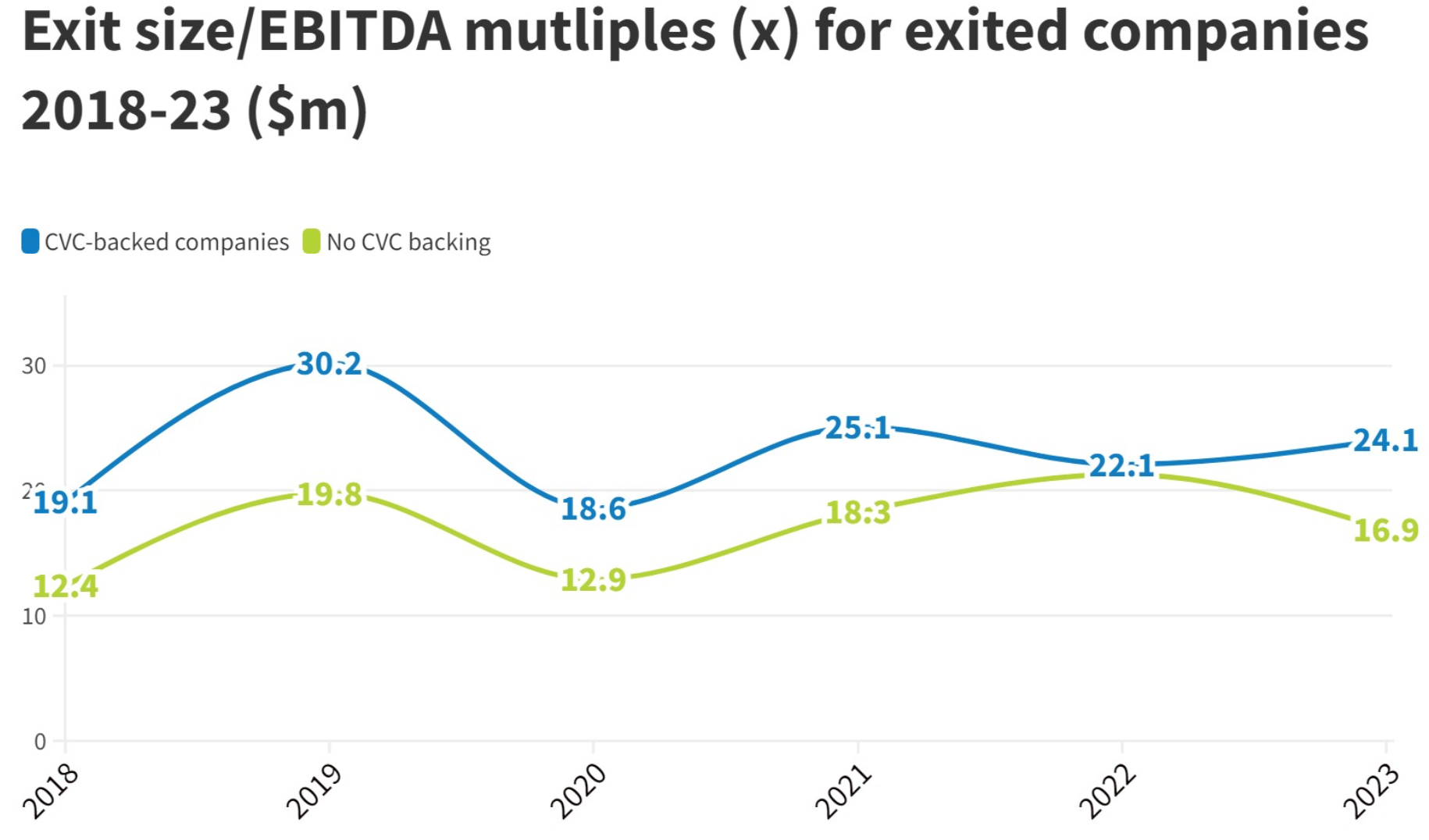

Startups with CVC investors exit at higher valuation multiples than those with only conventional VC investors.

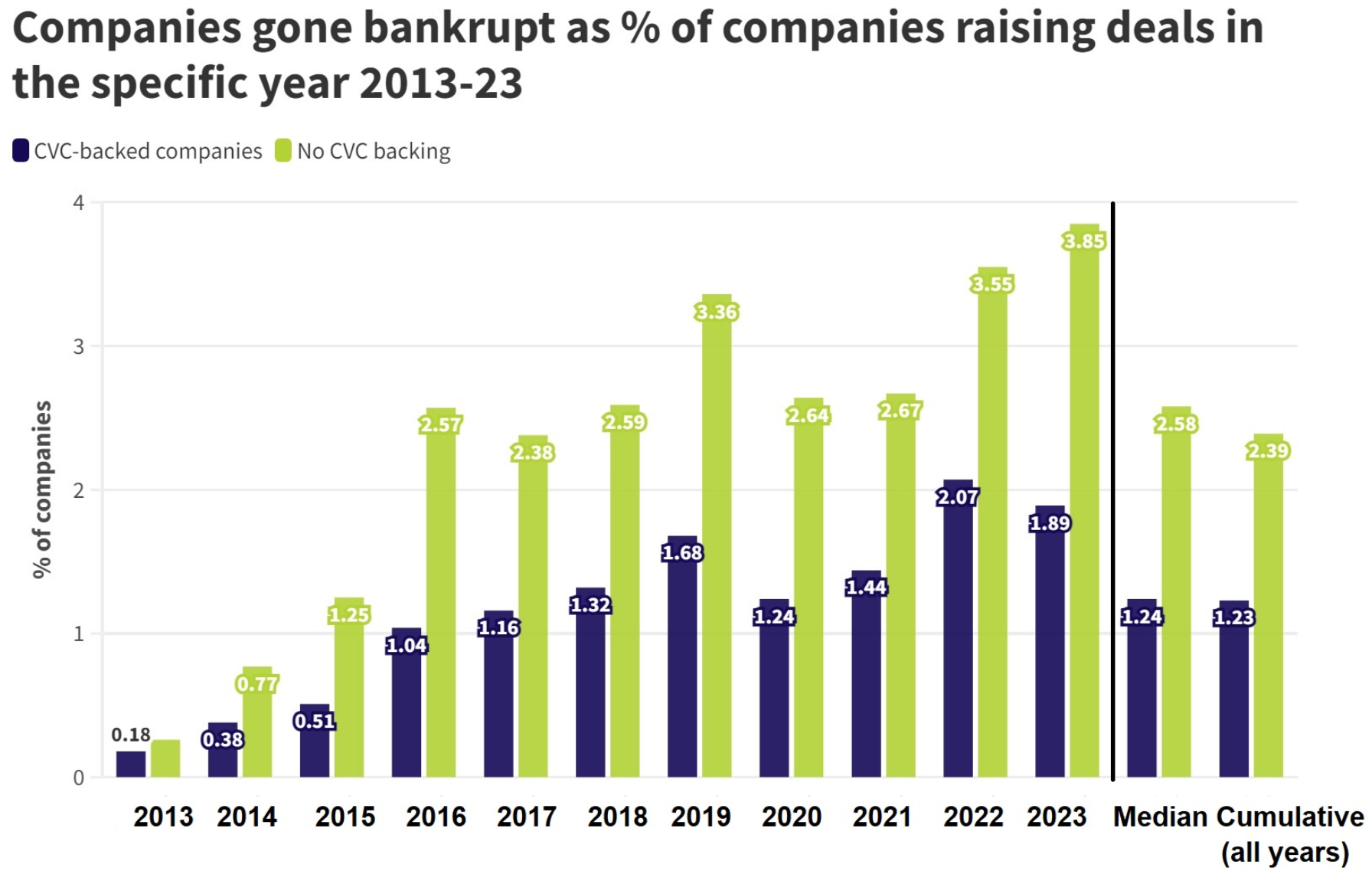

And the failure rate for companies backed by CVCs? It’s more than a third lower than for companies backed only by conventional VCs.

Why?

It may be because corporate investors have in-house expertise from the mothership to do a better job at technical diligence. That’s driven some conventional VCs to partner with CVCs to draft behind CVC’s diligence, as Foresight Group did in partnering with Williams Advanced Engineering of Formula 1 fame to evaluate Foresight’s deeptech investments.

Another explanation may be that CVCs can deliver commercial benefits to their portfolio companies, such as permitting the portfolio company to leverage the CVC parent’s sales distribution, that are hard for a conventional VC to match.

Perfect storm?

With attractive investment performance; CVCs looking for liquidity; and masses of dry powder from investors, we may be looking at historic growth in outside investment in CVC portfolios.

The attractive investment profile is why investors are increasingly chasing CVCs for opportunities to buy into CVC venture portfolios.

And with a dearth of M&A exits, and a quiet IPO market, CVCs are listening – they’re more motivated to seek liquidity events in nontraditional ways.

That’s why CVCs are getting more sophisticated about generating that liquidity by executing “strip sales” in which the CVC shares future upside with new investors, while getting a liquidity event today. The awkwardly-named “strip sale” is really a profit participation in which the CVC and the new investor share upside, but the CVC keeps its equity positions, keeps its governance rights, and keeps its commercial relationships. And because it’s actually a financing transaction, not a sale, it’s not a pricing event – and therefore it generally does not result in writedown for the CVC.

Executing those transactions is what we do – request a recording of our recent webcast on this topic here.

There’s also more capital than ever chasing secondary investments, with total fundraising surging by 180% in 2023, surpassing the combined total of 2021 and 2022. Near-term dedicated available capital for secondary investments is forecast to hit a new record of $255 billion, increasing the capital overhang multiple to 2.3x (meaning available investment capital is 2.3x the trailing secondary investment volume).

Plus, pricing on venture secondaries has now remained steady for two straight years, making buyers and sellers more willing to accept current valuations. All of that is driving a narrowing of bid-ask spreads, which facilitates deals getting done. And the portion of total secondary investment that’s going to venture capital (as opposed to private equity and other strategies) is up 50%, from 8% of the total, to 12% of the total.

So yeah – that’s why we expect a surge of investment from secondaries firms and other institutions, into CVC portfolios.

See our blog for more on this trend.

And reach out if a rapid, confidential “market check” to get a sense of your liquidity options makes sense for you, or if you’d like to schedule a one-on-one briefing.