We’re focused on software not just because it eats the world but because it’s a bellwether for VC generally as the single largest recipient of VC dollars, representing almost half of global VC investment. (By segment, generative AI and electric mobility blew the rest out of the water.)

So let’s look at SaaS valuations as a proxy for valuations of VC-backed startups generally.

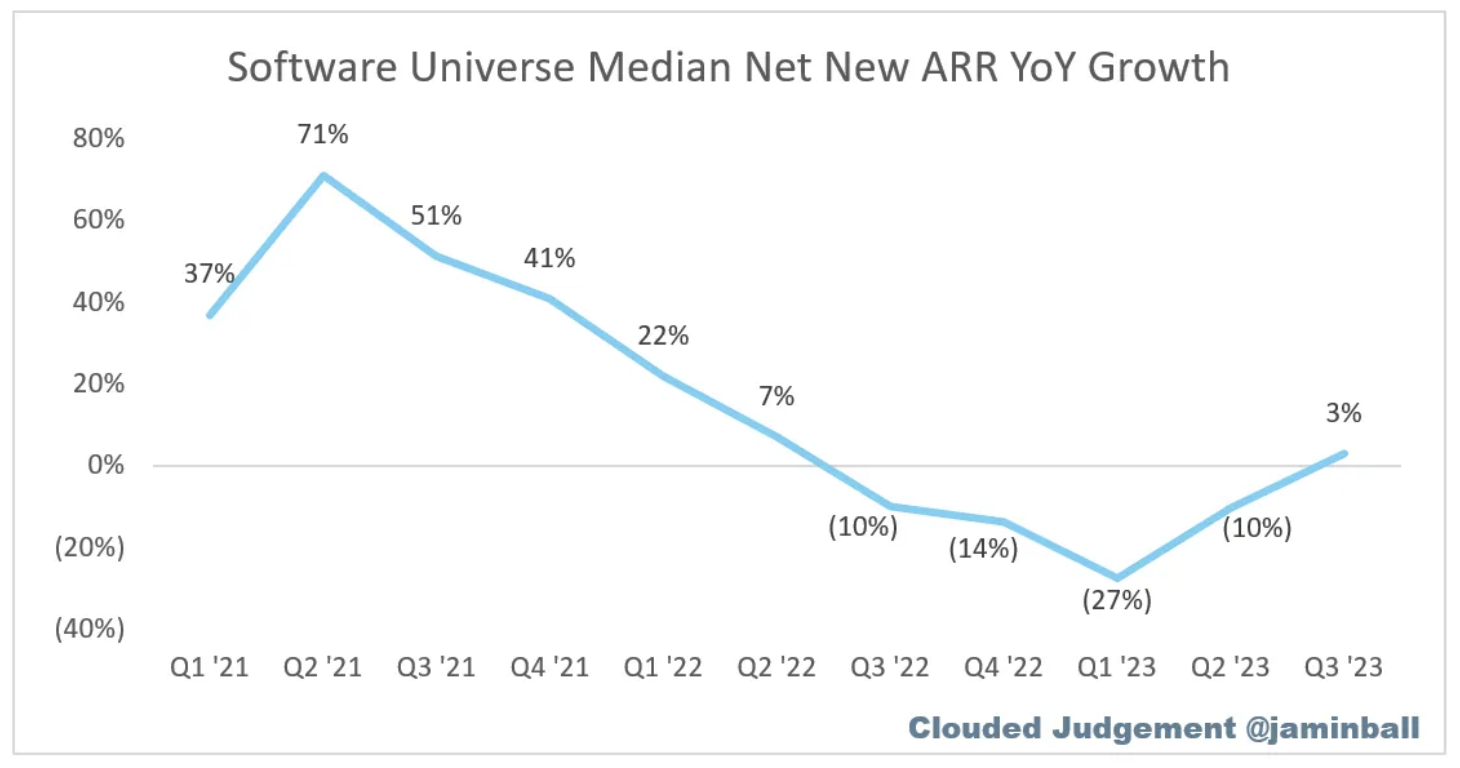

ARR growth went negative for 4 straight quarters starting in the back half of 2022.

Then, in Q3 2023: daylight. ARR growth turned positive.

What’s the impact on public SaaS valuations?

The long term pre-Covid multiple of next twelve months’ revenue (NTM) for public SaaS companies is 7.8x.

Could multiples rebound back to the long term average of 7.8x, assuming interest rates continue to come down, and ARR growth continues to go up?

Seems like.

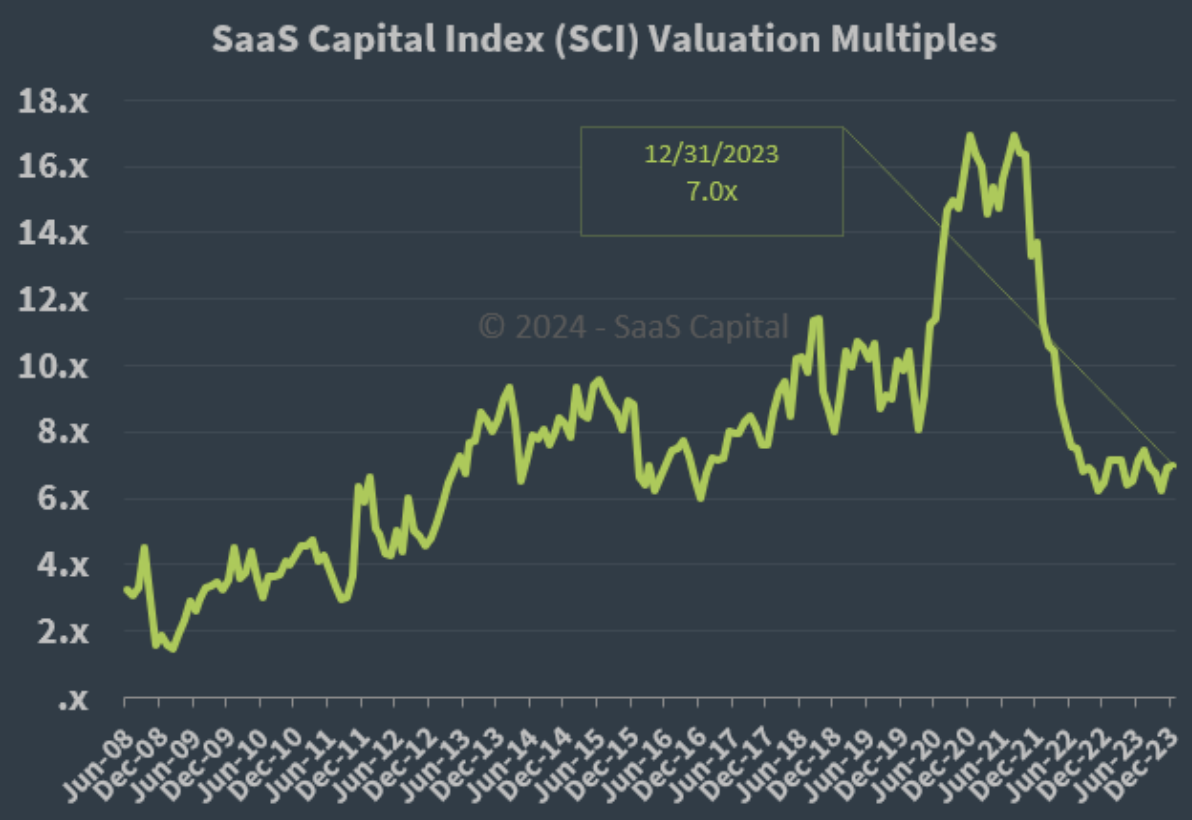

In fact, public company SaaS valuations appear to have turned the corner already. Or at least, they peeked around the corner and didn’t get their face shot off: The SaaS Capital Index, which reports valuations as a multiple of annualized current run-rate revenue (rather than next twelve months revenue, as many indexes do) has drifted up to 7.0x run rate ARR. That’s a long way from the 16.9x of August 2021 – but it’s a full turn higher than the most recent low of 6.2x in November 2022.

(That November multiple was the lowest multiple since the “flash-crash” of December 2016 when it hit 6.0x – which itself was the lowest multiple since Q1 2013 (5.8x) and marked the beginning of the nearly decade-long SaaS valuation boom.)

So, whither the private markets? (That’s whither, not wither.)

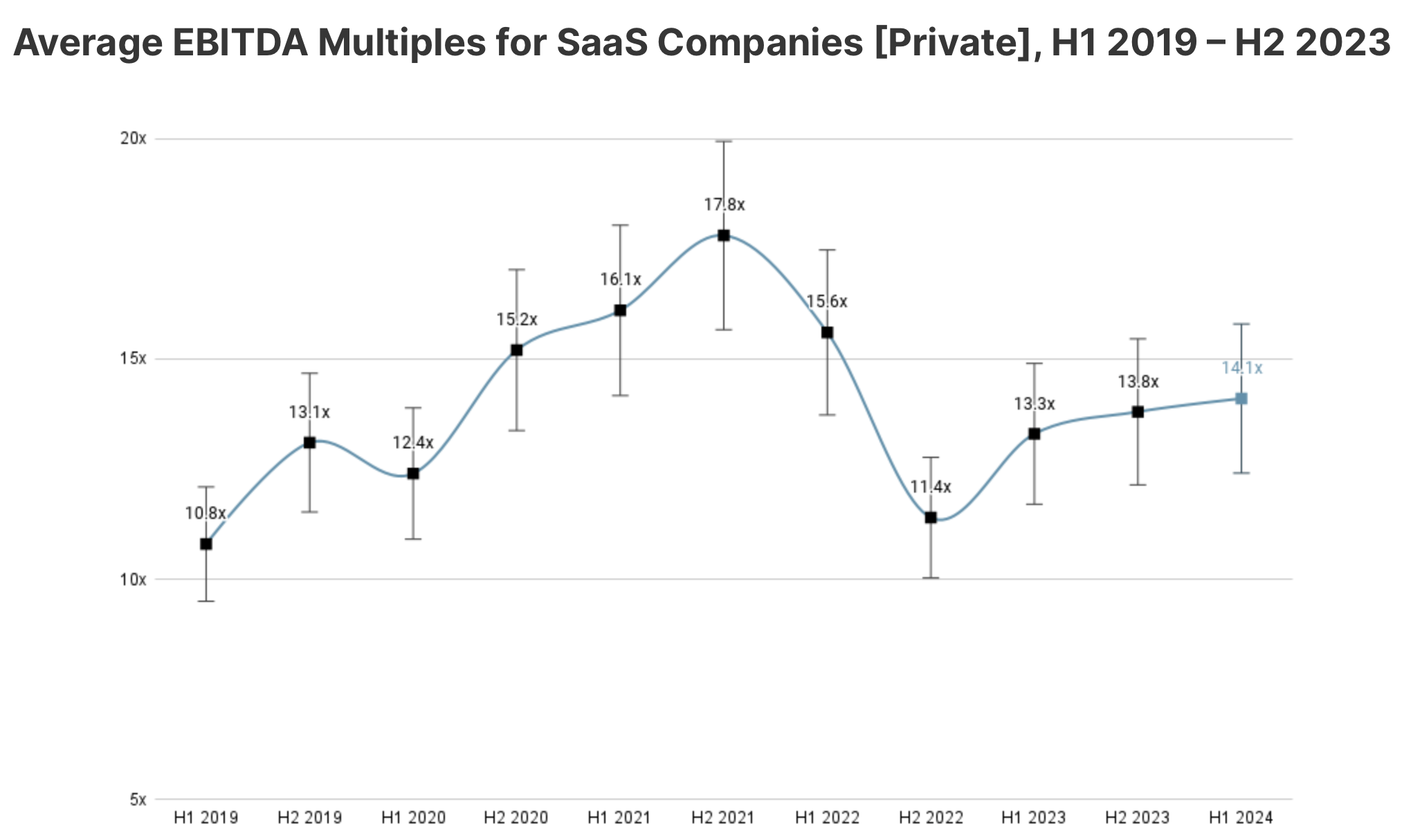

Private SaaS valuations have also rebounded.

They’re up from recent lows of 11.4x EBITDA, to 13.8x EBITDA, though they remain well below the high water mark of 17.8x in H2 2021. (Of course by definition, this EBITDA-based metric excludes unprofitable companies which skews the multiple upward relative to the broader universe of SaaS firms.)

In an example of the latency in the private markets, the bottom started falling out of public company SaaS valuations in the first half of 2022 and they had largely hit their lows by the beginning of Q3 2022. But private company SaaS valuations only began easing downward in the first half of 2022, dropped less precipitously than their public counterparts, and then took two more quarters to hit their lows.

What could spoil the party?

AI, for one thing.

Some people think AI will create headwinds for SaaS generally, including SPAC supervillain Chamath Palihapitiya. He’s betting that GPTs and similar tools will permit them to build 80% feature-complete versions of current SaaS solutions, at a 90% discount. Maybe that takes the wind out of SaaS sails. (And sales.) We’ll see.

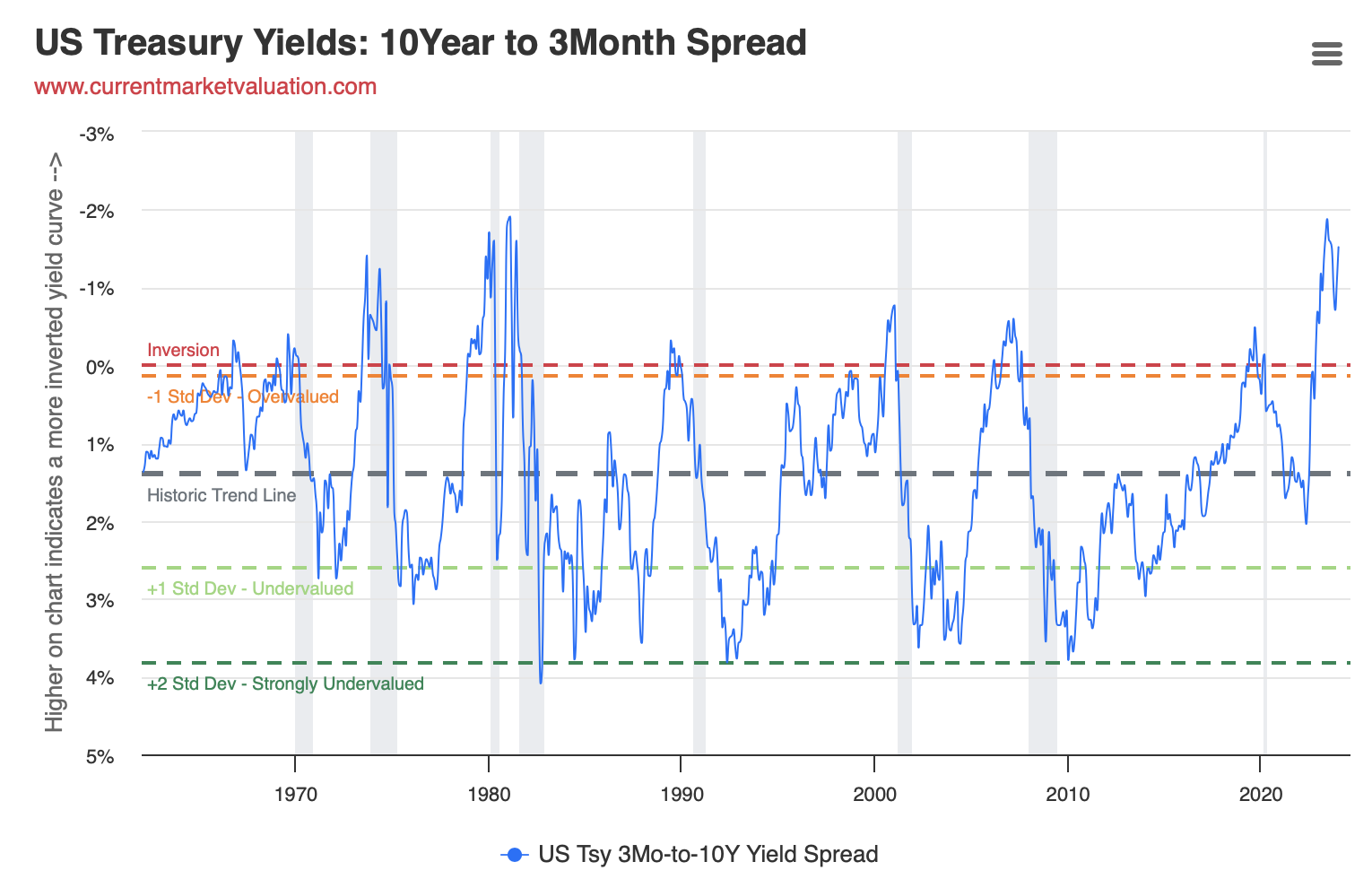

For another, the yield curve remains inverted.

What’s an inverted yield curve? Don’t ask the government to explain it. The Treasury helpfully clarified recently that it has begun “using a monotone convex spline method for deriving its official par yield curves and discontinued the use of the quasi-cubic Hermite spline methodology.” (Personally, I prefer Pete Holmes’s explanation on why nothing makes sense.)

Inverted yield curves are when interest on long term debt, is lower than interest on short term debt. In general, that shouldn’t make sense. If you want to tie my money up for longer, you should pay me for the privilege of doing so, by paying me higher interest.

But the curve is inverted now. Short term debt is yielding more than long term debt. It’s been this way since October 2022. And it’s generally considered a sign of bad news on the horizon, because it implies that investors expect lower interest rates are coming – for example, when the economy is expected to enter a recession and the Fed has to reduce rates to stimulate the economy. Another explanation for inverting, is that if investors expect a recession and declining interest rates, they try to lock in long-term yields, which increases demand for long term debt, driving up prices and reducing long term yields. It’s cited as having accurately predicted the last seven recessions, (though there are some suggestions that it’s become a “broken odometer”).

After briefly narrowing – and despite inflation declining, unemployment remaining low, consumer sentiment improving, and predictions of recession waning – the inversion is now widening again. The spread has doubled from 0.71% On October 31, 2023, to 1.52% at year end.

Does that portend that the long-predicted recession finally arrives, and take the wind out of SaaS sails/sales? We won’t try to call that. But we do take heart in improving fundamentals within the SaaS marketplace.

And as goes SaaS, so goes VC. So cross your fingers that the yield curve goes right side up again. (Uninverts? Deverts? Disinverts?)

And tell your boss (but maybe only sotto voce) that the software recession is over.