You invested in a bunch of startups. What are they worth?

That’s the $64,000 question.

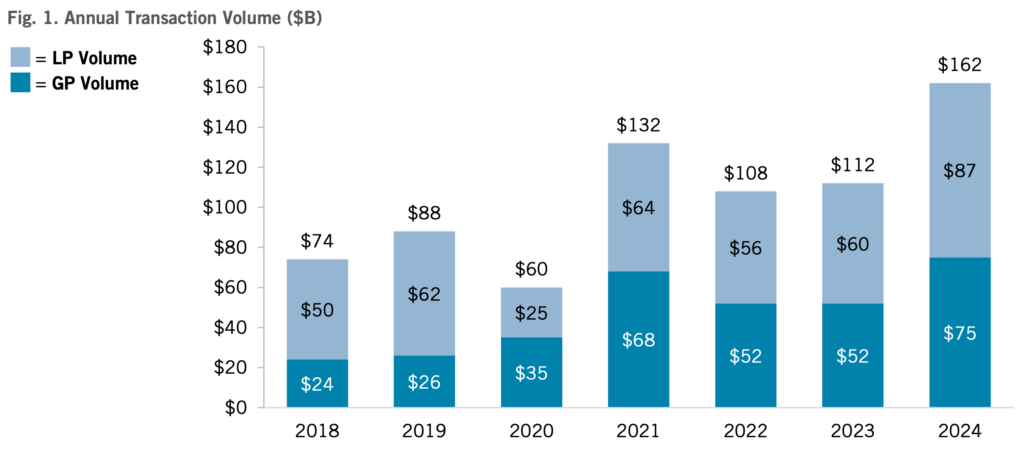

Actually that’s the $18,000,000,000 question. That was the volume of secondary investment in VC and other asset classes in 2024.

Absent a sudden surge in the IPO and M&A markets, generating liquidity in the secondary market remains many institutional investors’ best option.

And surging secondary volume continues to improve the outlook for generating exits via secondary sales and structured transactions.

Total secondary investment volume across all asset classes hit $162B in 2024, an all time record and a 45% YoY increase. Venture capital’s share of that total held steady at 11%. (PE remained by far the largest sector overall in dollar terms, but dropped considerably by share as the credit asset class more than doubled to 12%.)

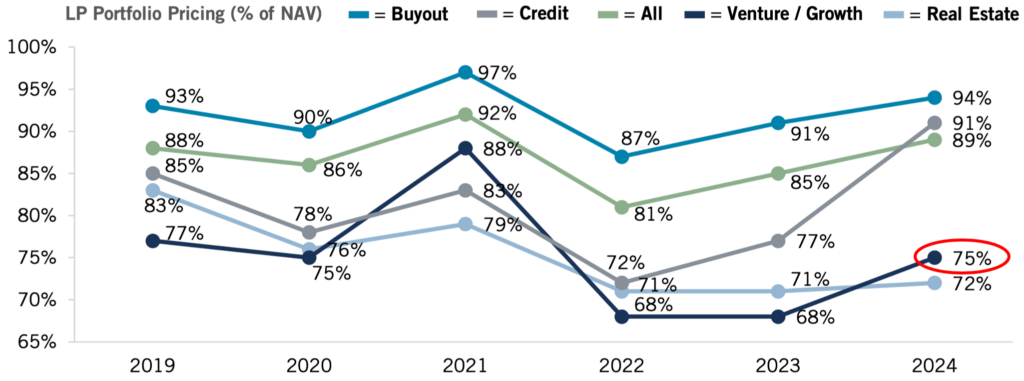

That surge in investment volume drove discounts down – and pricing up – across all asset classes.

In 2022, Jeffries drily proclaimed that the 2,000 basis point decline in venture capital pricing in the secondary market represented “the largest annual drop for any strategy in history.” That drop took pricing relative to NAV from 88% to 68%. It stayed there for the next two years, through 2023.

The headline number for 2024 is much more attractive: venture and growth equity pricing was up 700 basis points in 2024 to 75% of NAV, according to Jeffries.

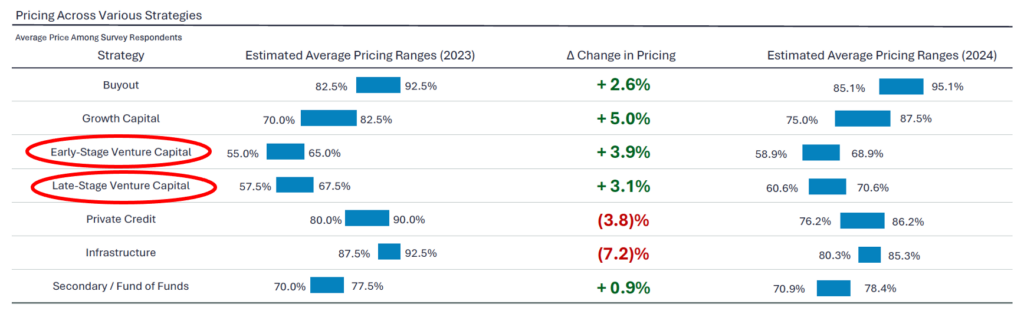

Lazard’s data set was less sunny; when excluding growth equity from the data set, venture pricing was estimated at 59% – 69% of NAV for early stage VC, and 61% – 71% of NAV for late stage VC.

But in both the Jeffries and Lazard data sets, valuations are up, and bid-ask spreads are narrowing.

(Some data sets show even smaller discounts. Zanbato reports discounts as low as 3% in some markets, though we believe that number is too skewed by retail investors piling into frothy names to have much predictive value for CVC investors.)

How do the headline valuations apply to your holdings?

We hate to say it depends. But, sorry, it depends.

Overall, the pricing data are likely skewed to the high side by secondary purchases at fizzy valuations in sought-after private companies like SpaceX and Anthropic which trade at small discounts or even premiums; and by strong valuations in LP positions in blue chip VC funds.

There’s no broad data on discounts that apply to corporate venture capital holdings, but in general, our experience is that they will shade lower than the market average. Generating liquidity at the top end of that discount range will depend on at least five factors.

How do you generate liquidity at the top end of the discount range?

To state the obvious, the single best indicator of value is how well the holdings are performing.

But generating exits at or above the discount ranges mentioned above depends on four additional factors that may be less obvious.

- Proximity to exit. Part of the secondary investor’s pitch to their LPs is that they will flatten the J curve by taking over equity stakes that are already partially seasoned, shortening the hold period, returning capital faster and increasing IRR. The closer your holdings are to ultimate exit, the more desirable they are to secondary investors and the smaller the discount.

- More NAV. Institutional secondary investors are often sitting on huge piles of dry powder. Coming to them with a single holding with say, $10mm of NAV, will often be too heavy a lift for them to diligence given the small ticket size. It’s different if the holding is a well known name. But if it is a more obscure company with less-known investors on the cap table, it will be a heavy lift to diligence and it will be hard to get attention and generate a competitive process. So, taking a package of assets to market with a higher total NAV to market will always improve the chances of generating real attention from secondary investors. There’s no magic number, but a portfolio of $25mm or $50mm of NAV will get much more attention than something below that bogey.

- More names. It’s not just maximizing the total NAV that you take to market in a secondary. It’s also maximizing the total number of names you take to market in a portfolio sale. There are exceptions where a portfolio is very diffuse by business vertical, geography, or maturity. Diffuse portfolios are a heavier lift to diligence, and are less likely to fit into a given secondary purchaser investment criteria. But in general more names in the portfolio generate more interest, in part because it increases the chance that there is a “lottery ticket” holding buried in the portfolio that may be undervalued but which generates an outsize return.

- More blue chip coinvestors. Finally, many secondary investors don’t want to get their hands too dirty in taking on your ownership positions and governance rights. Having other blue chip investors on the cap table credentializes the holdings with the imprimatur of well-regarded other investors. That can be especially beneficial where the seller is a CVC with a less-understood track record. But it also gives the secondary purchaser the comfort that they can draft behind the governance and strategic views of well-regarded incumbent investors who are already deeply versed in the company and will provide continuity following the CVC’s exit.

What could kill the buzz?

There are reasons to be cautious about whether the surge in secondaries will continue. More on that in our next post. But spoiler alert – not everyone is bullish on the deal making environment. For some it’s feeling like a roller coaster ride with an unknown destination.

“Nobody knows what’s up,” said one CEO. “It’s like being on Space Mountain at Disney World. You get on Space Mountain, you get in a car, and you’re in the dark and the cars go left and right, left and right and abrupt turns, you don’t know where you’re going.”

We’ll talk about how to strap in for that ride in our next post.