Let’s just say it hasn’t been the greatest time to be a VC. Exit volume has been dismal for three years running.

1. An IPO boom will fix everything. Right?

Welp, not so far.

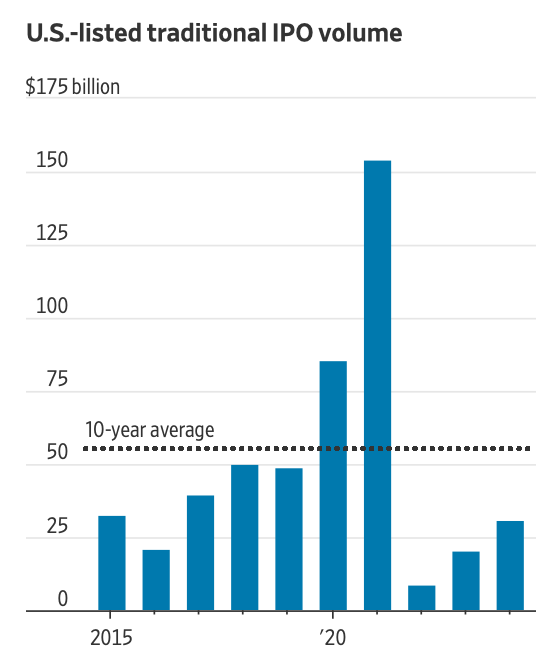

IPOs have cratered since 2021. The aggregate value of the 2,040 exits in 2021 totaled $841.5 billion—almost 6x the number posted in 2024.

Even with slight growth in 2024, IPO volume remains far below the 10 year average. Q3 had only 14 public listings and a median exit valuation of $129mm, less than half the YTD median of $292mm. All the venture-backed IPOs in the quarter originated from the healthcare sector – and none crossed the billion-dollar valuation threshold.

The anemic IPO market is one reason that IPOs are just becoming less important as means of generating liquidity.

Another reason IPOs are less important is that companies are staying private much longer – in fact, more than 10 years, for D round companies. These aren’t the liquidity timetables most GPs promised.

That’s why so many companies are bypassing IPOs through secondaries and tender offers to generate liquidity, that the WSJ cheekily declared IPOs Are So Passé. More on that later.

Okay, well acquisitions will fix everything?

Not looking good.

M&A exit valuations of venture-backed firms are very low YTD, at a $150 million median. And even that figure may be high given that over 85% of 2024 acquisitions had small and therefore undisclosed deal sizes, likely biasing the median figure higher.

M&A exit volumes are low too – and very concentrated in healthcare. Only two exits in Q3 exceeded the billion-dollar threshold, and both were for biotechnology companies. In fact, the top five acquisitions by size all came from healthcare, another indicator that overall venture M&A activity has not returned.

Okay fine – but won’t rising valuations in venture fix everything?

Big picture valuations look good by some measures. But the overall data is heavily skewed by AI mania. One example is AI research lab Safe Superintelligence raising $1 billion for its very first round at a $4 billion premoney valuation.

Those headlines and data points swamp the broader reality that 2024 venture-growth medians were a mere $5.5 million in deal value.

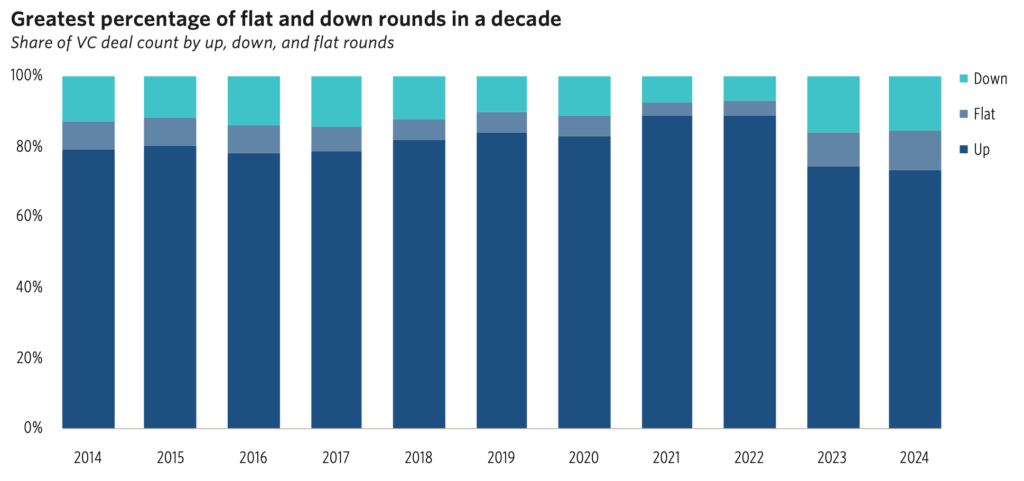

In fact, the combined percentage of flat and down rounds is at a decade high of 26.6%.

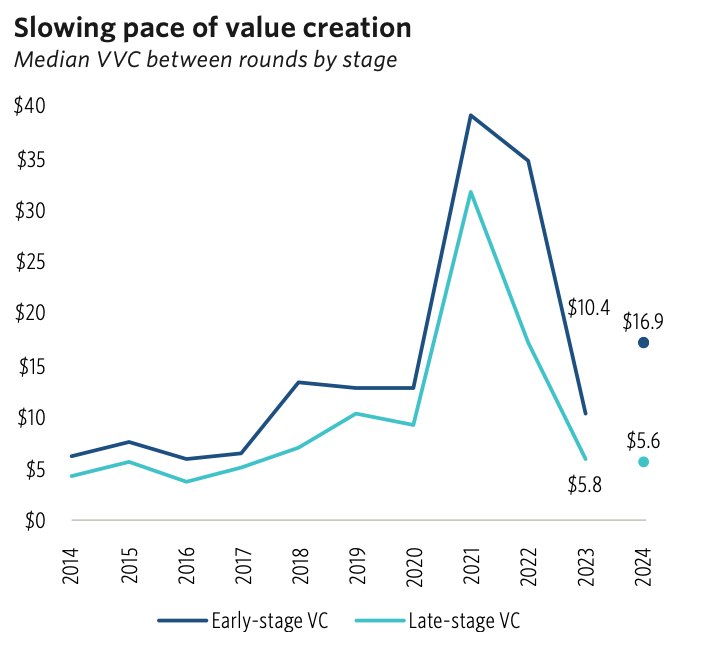

The delightfully wordy “relative velocity of value creation” (RVVC) metric is instructive. It measures annual growth in valuation between rounds. RVVC has gotten crushed since the ZIRP era as valuations reset to more reasonable levels.

The median RVVC in early-stage companies is now 35.1%, a 74.5% decrease from 2021’s RVVC and the second-lowest level in the past 10 years. Later-stage median RVVC is similarly at a decade low of 11.3%, an 83% decrease from 2021.

So – falling interest rates, then? That will fix everything?

Don’t get us started. They’re going the wrong way, fast.

We don’t recommending staking everything on the hope that what everyone “knows” will happen in the future, will actually happen. Falling interest rates, falling inflation, rising IPOs? They’ve been confidently predicted for two years now. Along with recession.

Our view is that no one knows anything on these macro indicators.

All of which explains why secondaries are so hot.

So what’s the answer to how VC will generate liquidity in 2025? Secondaries, tender offers, and other non-traditional paths to liquidity.

The market data agrees. We don’t have full year 2024 data yet. But global secondary volume was $68 billion in H1 2024, a 58% increase from $43 billion in H1 2023. And tender offers are up 10x on the NPM platform since 2013.

Total dry powder for secondaries (including available leverage) is at a record $253 billion, and projected 2024 deal volume was just revised upward to $140 billion.

The supply of new secondary capital is very large.

The demand from VCs for liquidity is also very large.

Unlike PE investors who generally have control positions and can dictate exit timing, VCs are usually minority investors and have until recently, been more passive about generating liquidity.

That’s changing. 52% of corporate venture arms have considered using secondary markets and 15% have already done so.

All of that is driving a surge in volume for VC secondaries. 14% of the total $140 billion secondary deal volume is now going into venture. That’s up from 5% in 2020. (For context, the $20 billion that went into venture secondaries in 2024 is more than the total secondary investment that went into all asset classes combined – venture, private equity, real estate and credit – in 2008.)

And the surge in transaction volume is bringing a recovery in VC secondary pricing.

Relative to their last funding round, prices of direct secondaries have gone from trading at an average discount of 50% in early 2023 to 12% by September 2024 (though this data set is skewed toward the highly desirable private companies that trade on Zanbato such as SpaceX and Databricks).

So our counsel: don’t trust people who know everything, and assert that IPOs and M&A are going to come roaring back. And that interest rates are going down. And that the Buttered Popcorn Index is bullish.

For VCs looking for liquidity, the secondary market is where the deals are happening.

VO2 Partners is a boutique advisory firm that delivers liquidity for institutional VC investors. Whether it’s driven by reducing balance sheet volatility, topping up dry powder, or increasing focus by divesting non-core holdings – that’s what we do.